Background

There has been a lot of discussion about tariffs post-election, and a simple tweet caused the currency markets to erupt. So, if free trade has been so good for us, why are tariffs even on the table?

Firstly, I should admit some bias. I am a huge proponent of free trade. My father was instrumental in fighting for it and in negotiating the FTA and NAFTA. But like many things in life, this is not a simple issue. Canadians should prepare for at least four years of an America First agenda.

Tariffs make for good politics. Trump’s base in the northeast, the Rust Belt, was instrumental in returning him to power. Many blue-collar workers were vocal in their support for Trump, who made a significant commitment to protecting US manufacturing. While this won’t go away any time soon, it is important to gauge the why and how of the vision for trade barriers.

Trade Surplus Versus Deficit

An excessive trade surplus is not as good as it might seem. Superficially, a surplus suggests a competitive production process. A stronger currency should balance the books over time. However, if the general objective is to build up USD reserves, the currency is less likely to adjust, and the competitive edge is more likely to be sustained. As a result, there is no immediate need for productivity improvements. The capital has moved to a foreign jurisdiction. As a result, it puts upward pressure on debt to finance investment growth.

An excessive trade deficit is the other side of the coin. It necessitates productive use of capital in the face of a strong currency. However, it unfortunately creates downward pressure on wages to support the return on capital. The strong dollar facilitates the consumption of foreign goods and services because they seem cheaper each year (relative to domestic goods and services) which dampens the impact on blue-collar workers. The result seems like these workers are losing the financial benefits of productivity gains to the foreign capital invested in their companies.

Enter Trump

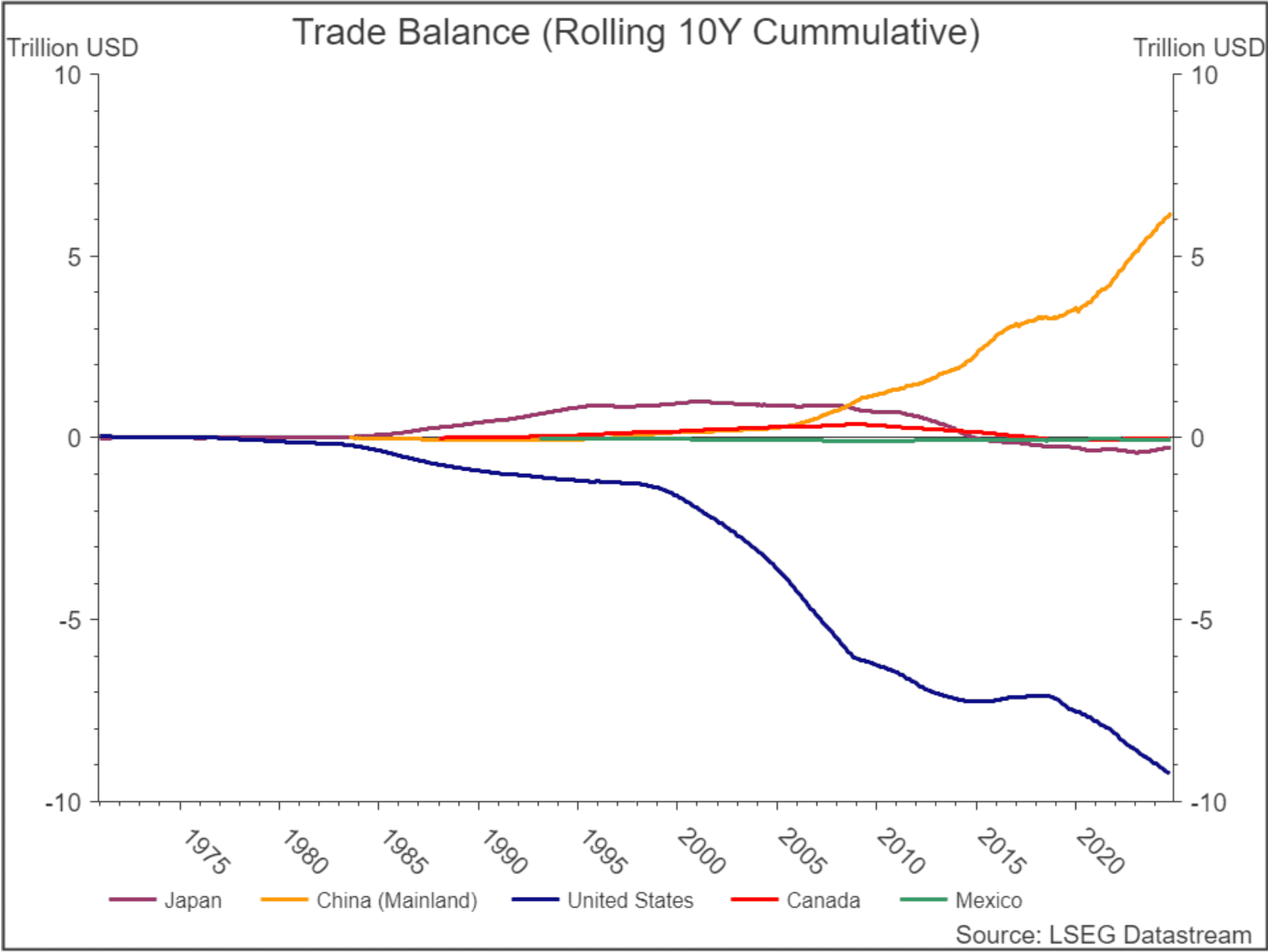

If the world wants US Dollars to invest in US financial markets, then, they must sell goods and services to Americans to acquire those dollars. The net effect of the world investing in US financial markets has been higher debt and a suppressed American worker (who collectively voted for another four years of Trump). The outcome of the American election demonstrates the importance of this issue. Chinese trade policies are designed to acquire and hold USD, which serves to manage or manipulate the Yuan. This isn’t new either. The Japanese used this approach for 25 years before them. In Trump’s crusade, Canada and Mexico are collateral damage rather than the problem in isolation (see chart). But good politics don’t need to be precise, they need to enhance MAGA wins.

Graph of selected cumulative trade balances over rolling 10-year periods.

Takeaways

Protectionist policies are not growth-friendly. De-globalization adds stress to supply chains, and alternative suppliers take time to ramp-up capacity. Inflation will likely surface in both the cost of goods as well as broad labour costs, manifesting in service inflation. It also suggests a shift of economic value back to labour from capital. Watch for a reaction in automation and robotics using machine learning. It is not just a matter of adding tariffs. This is all about fair trade and Canada needs to advocate for Free and Fair Trade.

Follow us on LinkedIn to stay up-to-date.

The information contained herein has been provided by GB Wealth Inc. and is for information purposes only. The information has been drawn from sources believed to be reliable. It is not intended to provide legal, accounting, tax, investment, financial or other advice and is not to be construed as a recommendation to buy or sell. The information contained herein may constitute forward looking information. Forward looking information is based on assumptions and subject to risks and limitations. GB Wealth Inc. is not liable for any errors or omissions in the information or for any loss or damage suffered. The GB Wealth logo and other trademarks are the property of GB Wealth Inc.